Treasury Bills

Treasury bills (T-bills) are bonds issued by the US government. The idea of bonds is that the party buying the bond at a given price gives a loan to the bond issuer (the government) to finance some activity, expecting to get regular payments called coupons at a specified rate as well as the original loan in full at a pre-determined expiration date, known as maturity.

T-bills have different time-to-maturity e.g. 3 months, 1 year, 10 year, 30 years. The 10 year T-Bills is one of the most monitored bonds and has implications for the global economy as a whole as it serves as an indicator of the underlying sentiment in the economy and in particular on the expectations for the future.

Why? The government bonds are considered risk-free, the government will always pay back the bond in full and meet the coupon payments, because it’s backed by the US government. Therefore that’s the safest, risk-free investment one can make. Therefore the more interest there is in these bonds, the more safety or risk averse investors are meaning, they prefer safe bets, and don’t believe in significant economical growth, i.e. are pessimistic. Conversely, if there is little demand for the bonds, it means investors believe they can get higher returns elsewhere, in riskier investments, indicating optimism in the economy.

The bonds are sold through bidding and therefore their prices are determined by demand, higher demand higher prices, lower demand lower prices. The coupon is given as a pre-determined percentage of the bond value when it was issued. The yield of the bond, is the coupon value (pre-determined) as a percentage of the current bond with the given maturity (e.g. 10 years) price. In particular, if the bond price goes up, the yield goes down and vice versa, an inverse relation.

The causal chain is:

Optimistic view -> Lower demand for 10-year T-bills -> T-bill prices go down -> 10-year T-bill yield goes up.

Pessimistic view -> Higher demand for 10-year T-bills -> T-bill prices go up -> 10-year T-bill yield goes down.

Another important T-bill is the 3-month T-bill, i.e. 3-months to maturity. For a bond to be profitable for investors it should have a yield at least as high as current interest rate given by the Federal bank, otherwise one can get higher returns simply from the interest rate of the bank. In that way the interest rate plays a role in the bonds’ coupon rates. Typically the shorter term bonds have lower coupon rates because the risk of lower risk of the interest-rate changing unfavorably, as opposed to the 10 year bonds in which there is higher risk, and therefore to compensate the risk the yields are higher.

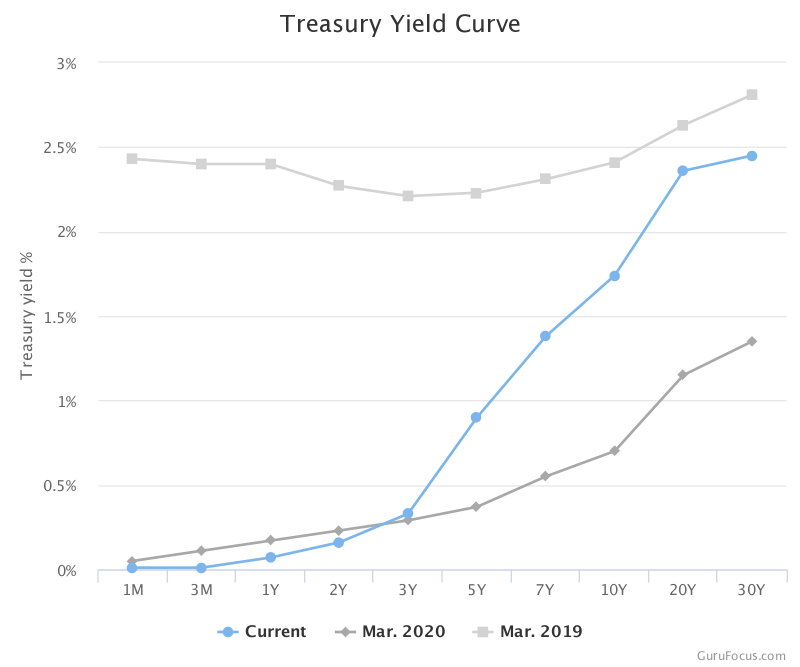

An important indicator chart and corresponding indicator is the yield curve, which shows the yields for different bond maturities. It has important implications on the future expectations of investors on the economy. The most common derived indicators from the yield curve are obtained by taking the difference of the long term and short term yields, typically the 10-year and 1-year or 3-months yields, which are known as the 10-year 3-month yield spread, or just the yield spread.

https://www.gurufocus.com/yield_curve.php

A normal yield curve will have higher yields for higher maturities because of the higher risk of holding a bond for longer time with fixed coupon rate. The normal yield curve indicates expectations of economic growth, potential inflation which will eventually lead to the short-term interest rates to increase.

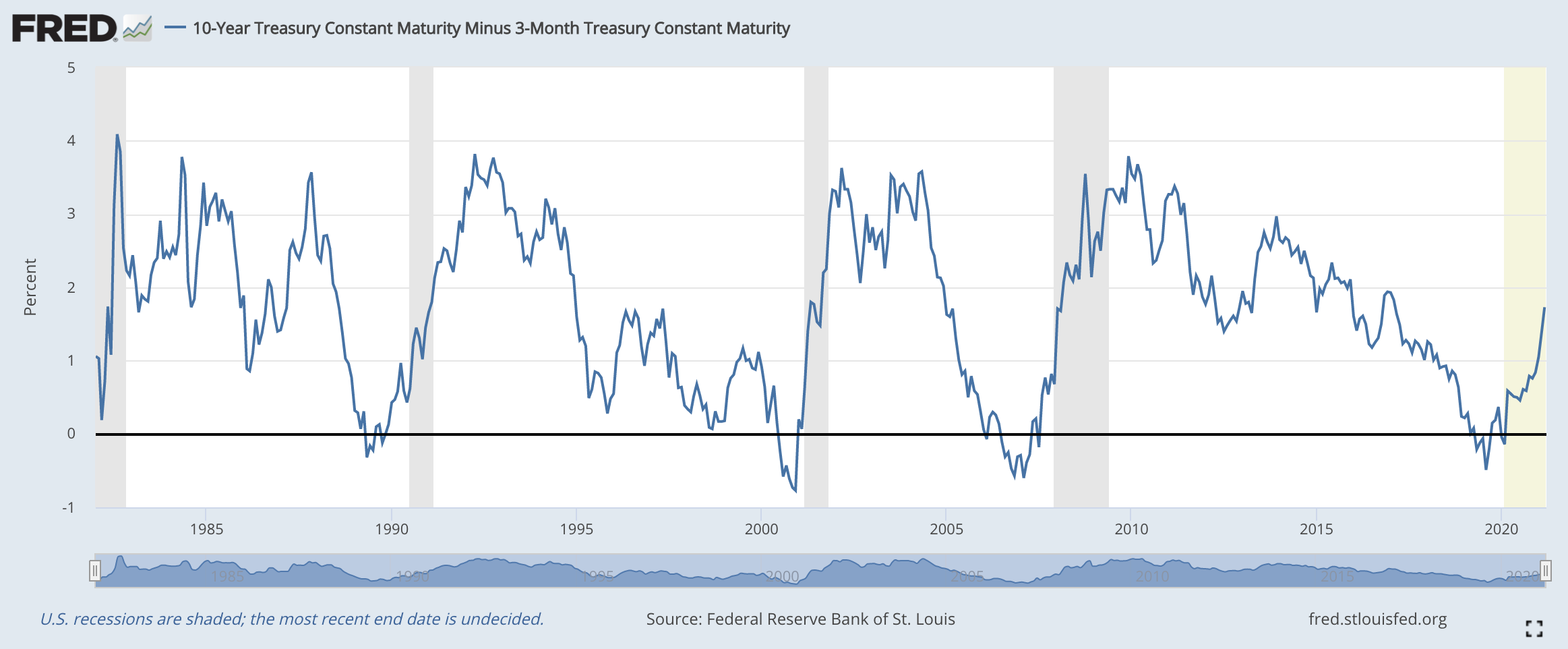

The most interesting case occurs when the yield curve inverts, i.e the spread becomes negative. This occurs when there is high demand for the long term bonds due to pessimistic views on the future economy, in particular rising short-term interest rates and slowing down of the economy, with expectations that eventually interest rates will fall, leading to higher yields for short term maturities compared to long term and inverting the yield curve. The inverted yield curve, or negative spread has historically been an accurate predictor of recession in the year following the inversion.

Source: https://fred.stlouisfed.org/series/T10Y3M

The chain of events is as follows: Expectations of recession and a corresponding reduction in interest rates to stimulate economy -> long-term bonds are in higher demand -> long-term bond prices go up as long term bonds are more appealing, providing higher returns than doing nothing -> long-term bond yields go down -> yield curve inverts -> recession occurs

Note that the arrows above are not causal, but are both driven by common drivers that lead to the correlated behaviour, the key being that the expectations of the market as reflected by the bond yields is a good predictor (the market knows best) of the future economy.